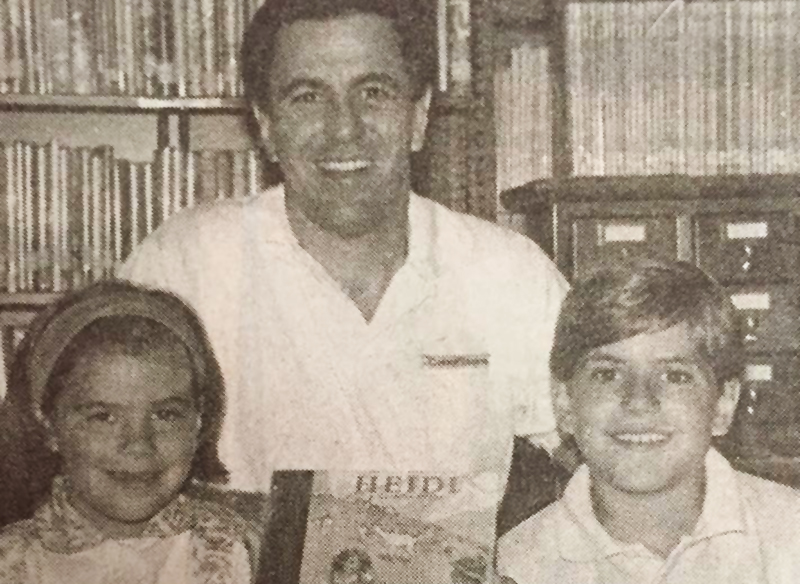

After losing his wife, Heidi, to leukemia, Victor and his children, Abby and Adam, didn't have to worry about losing their home. Life Insurance provided much-needed security during a most difficult time.“There are two basic motivating forces: fear and love,” John Lennon once said. “When we are afraid, we pull back from life. When we are in love, we open to all that life has to offer with passion, excitement and acceptance.”

After losing his wife, Heidi, to leukemia, Victor and his children, Abby and Adam, didn't have to worry about losing their home. Life Insurance provided much-needed security during a most difficult time.“There are two basic motivating forces: fear and love,” John Lennon once said. “When we are afraid, we pull back from life. When we are in love, we open to all that life has to offer with passion, excitement and acceptance.”

The late Beatle probably wasn’t thinking about insurance when he said that, but I find Lennon’s words particularly applicable to one particular type of insurance: Life Insurance.

While some may be driven to purchase a policy out of fear for what might become of their family if sufficient financial protection were not in place, love to me is the greater motivator. I encourage clients to purchase Life Insurance not to insulate themselves from fear, but rather to invest in the promise of their loved ones’ future. And when you look at it that way, purchasing Life Insurance really is something to be done with passion, excitement and acceptance.

That’s why I prefer to think of it as “Love Insurance.”

I know that’s the way my father-in-law sees it.

Victor’s story

Victor, my father-in-law, first purchased Life Insurance not long after he and his wife, Heidi, got married — in part because he thought it was just something married couples should do and in part because some co-workers recommended their local independent agent. But it was a few years later, after they purchased a house, that he first really thought about why having Life Insurance was important.

“I realized it took two incomes to pay the mortgage,” Victor recalled. “I thought, What if something happens to one of us? We’re not going to be able to keep this house.”

Victor’s first inclination was to purchase mortgage insurance, but his agent had a better solution: 20-year Term Life Insurance policies. Because he knew his clients and understood their needs, the agent also added a rider to the policies, which stipulated that there would be no premium on the policy if the named insured became disabled. When the agent learned that Heidi had been diagnosed with leukemia and could no longer work at the paint store she and Victor owned, he called Victor to express his support and remind him that the premium on Heidi’s policy was now covered due to her disability.

By this time, Heidi and Victor had two young children. And though nothing could compensate for the loss of their wife and mother, the grief Victor and the kids experienced was at least mitigated by not having to worry about losing their home.

“It was awful enough having to deal with losing Heidi,” Victor said. “When it did happen, I knew that losing our home was not a concern because there was Life Insurance in place to help pay the mortgage. Having two children, losing their mother was terrible. But to lose their home too? Life Insurance at least allowed us to continue on in the same lifestyle, and that was huge — huge.

“You think it’s never going to happen to you,” Victor continued. “But to have that protection when your whole life has been turned around and thrown into turmoil — your losing your wife and your children losing a parent — at least your life can go on otherwise seamlessly day to day. Paying the mortgage was absolutely one less worry I had to concern myself with.”

Life Insurance basics

September being national Life Insurance Awareness Month, there’s a good deal of promotion right now about the importance of life insurance. And, with the nation still under the cloud of a deadly pandemic, some of that promotion seeks to capitalize on fear. But, as certified financial planner and “Future Rich” podcast host Barbara Ginty recently told CNBC, “I only would recommend buying life insurance if you have a need for life insurance.”

The CNBC post in which Ginty is quoted sums up who needs life insurance nicely:

“Generally, the questions to ask yourself before buying life insurance are: Will there be a financial hardship for your loved ones if you pass away? Do you have a spouse, partner or child depending on your income? Did you buy a home with a spouse or partner that is based on two incomes? Did a parent co-sign a student loan that will not be discharged if you die?”

As outlined on the Life Insurance page on the Sylvia Group website, Life Insurance includes two basic options for addressing those concerns: Term Life Insurance and Permanent Life Insurance, with the latter subdivided into two kinds of policies — Whole Life and Universal Life.

What’s best and how much?

What kind of Life Insurance policy is best for you, and how much insurance do you need? There are many factors to consider, such as:

- your age and the age of any dependents

- what outstanding financial obligations you have

- whether you want or need the flexibility of a policy that can provide cash while you’re still living.

Among the available “living benefits”:

- Tax-deferred growth. When you have a permanent life insurance policy, the cash value grows tax-deferred.

- Loans. You can borrow against the cash value of your policy for things like tuition payments, emergencies and even to supplement your retirement income. Keep in mind, this still is considered a loan, and if it’s not repaid before you pass away, then your death benefit is reduced by the amount of the loan plus any outstanding interest. Also, failure to pay loan interest could result in the policy lapsing.

- College savings. If you have kids who will attend college someday, your life insurance cash value could be used to help pay for their schooling and it is currently not considered in federal financial aid calculations.

There’s no one-size-fits-all solution, which is why it’s best to have a conversation with an agent who knows Life Insurance — someone who will listen to your questions and concerns, talk with you in basic, straightforward terms and instill a sense of confidence that you’ve purchased coverage that meets not only your needs but the needs of your loved ones. Someone, in short, who understands the concept of “Love Insurance.”

By KRISTEN EDWARDS

Account Executive, Sylvia Group

CONTACT KRISTEN

About Kristen Edwards and Sylvia Group

Well before joining Sylvia Group as an Account Executive, Kristen Edwards had built a strong working relationship with the Dartmouth, MA-based insurance, benefits and financial services agency. In various roles at such highly regarded companies as Blue Cross Blue Shield of Massachusetts, Allways Health Partners and New York Life, she had come to recognize Sylvia Group as an organization that shares her values of industry expertise and attention to detail, along with a passion for client service.

Kristen’s role as a member of the Sylvia Group team enables her to put her diverse background in the carrier side of the insurance and benefits industries to work meeting the diverse needs of the agency’s clients. In addition to Life Insurance, her specialties include: individual and group financial services, Long-Term Care Insurance, retirement planning and employee benefits.

Sylvia Group empowers businesses and individuals with performance-based insurance, benefits and financial planning programs. We make our clients active participants in managing risk and containing premiums, resulting in coverage that is both customized and cost-effective. In addition to making a difference for our clients, we make a difference for our community as a whole by actively supporting and serving many of southern New England’s most reputable and effective nonprofit organizations and institutions. At the outset of 2020, Sylvia Group became an Alera Group company, combining the local, personal service for which we’re known with the scope and resources of a national firm.